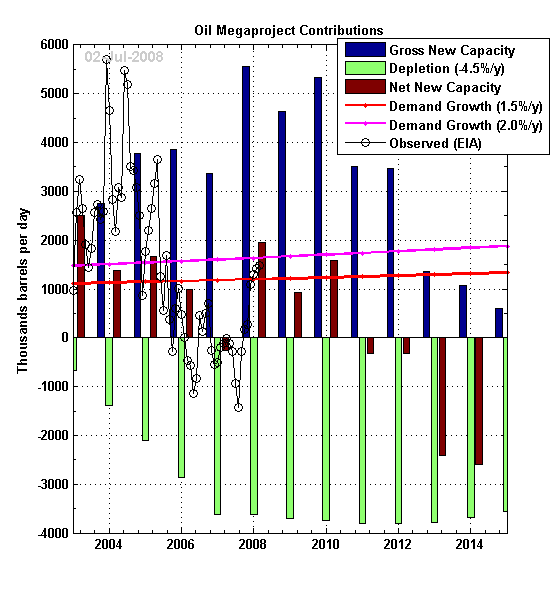

This is an update on the Wikipedia Oil Megaproject Database maintained by the Oil Megaprojects task force (Ace, Stuart Staniford, myself and many others). The database contains now more than 425 separate entries and is growing everyday. Despite the database growth, the outcome seems to become more pessimistic with time. The derived net new capacity (i.e. once depletion from existing production is included) is around 1 mbpd until 2010 with a jump at 2 mbpd in 2008 then depletion may dominate.

Possible future supply capacity scenario for crude oil and NGL based on the Wikipedia Oil Megaproject database. The resource base post-2002 decline rate is a linearly increasing rate from 0% to 4.5% between 2003 and 2008 then constant at 4.5% afterward. The decline rate for each annual addition is 4.5% after first year.

[break]

Below is the evolution of the new supply additions since the beginning of the project compiled by year of first oil:

December 2007

January 2008

February 2008

March 2008

May 2008

June 2008

We can clearly see the initial 2008 and 2009 peaks wearing out with time due mainly to delays. Now the situation does not look so good:

Possible new gross and net new supply additions compiled by year of first oil. Crude oil + NGL monthly production from the EIA. The resource base post-2002 decline is a linearly increasing rate from 0% to 4.5% between 2003 and 2008 then constant at 4,5% afterward. The decline rate for each annual addition is 4.5% after first year.

Below is a possible scenario for future supply assuming a 4.5% decline rate.

Possible future supply scenario for crude oil and NGL based on the Wikipedia Oil Megaproject database. The resource base post-2002 decline is a linearly increasing decline rate from 0% to 4.5% between 2003 and 2008 then constant at 4.5% afterward. The decline rate for each annual addition is 4.5% after first year.

This scenario seems to agree with this recent statement from Ray Leonard:

“By 2010, the production of the fuel that has driven the world’s economy will start to rapidly decline. This will conflict with the steadily increasing demand for oil. The collision of these two trends will lead to shortages and increased prices, providing a strong incentive to shift to alternative fuel resources…Due to unequal distribution through the world of oil and gas supply and consumption, [the upcoming] transition will result in significant shifts in global power and wealth.”

Many thanks to Ace who has diligently updated the data and put more than 500 separate contributions.

Finally, maintaining this database is a lot of work and it is crucial to track delays, project final approval, etc., so I'd like to repeat our appeal: the more folks in the TOD community head over to the Wikipage and help, the faster we'll know what's really going on here.

Related stories:

Update on Megaproject Megaproject

Help us List Megaprojects

[From Oil Megaproject Update (July 2008)]

Thursday, 3 July 2008

Oil Megaproject Update (July 2008)

Monday, 30 June 2008

Answering the Comfortable Questions about Energy

There is an old vaudeville skit that has an actor (Annie) come on stage behind the M.C. and begin visibly searching the floor of the stage. “What are you doing, Annie?” asks the M.C. “Looking for my ring,” she says. So they both start to look over the floor. After a while the M.C. looks at Annie and asks “Where did you lose it?” “Backstage,” says Annie. “Then why are we looking for it out here?” asks the M.C. “Because it is too dark to see backstage,” says Annie.

I was reminded of this skit as I watched a ”panel of experts” on the PBS News Hour with a couple of energy analysts talking about petroleum economics, and the cause of the current price rise. Their reasons (one blaming it in part on the Federal Reserve decision to cut interest rates) related to their areas of expertise and knowledge in the Commodities Markets. It is a common failing. Experts will try and explain events or seek to control events, based on their what they know and are comfortable with discussing (where it is light), rather than necessarily going to the root cause of the problem (where the ring was dropped). It is a fault both of those who select the experts to give an opinion, and the focus of those experts, and where this approach is used extensively it tends to hide the nature of the true problem from the public, in the obfuscations of those who are comfortable only when turning the question to allow answers that relate to subjects they know about.

[break]

In the current debate about why the price of oil is going up and what can be done about it, the current cause is often cited as being due to “speculators who play the market out of selfish interests.” And in the PBS discussion there was the suggestion that traders had increased the value of oil perhaps $30 - $50 dollars over the true price. Yet while the analysts concentrate on this “market factor” they ignore the underlying increase in price that has lifted the price the majority of the way to its current level. Because they (and many other analysts) are more comfortable talking about stock market factors, this is where they focus their discussion and the blame for the current rise in prices. And, because they don’t really understand the reality of the current situation, there are comments such as that in the Economist which advises

In theory, the world still has a little more spare capacity, in Saudi Arabia. The latest increase will raise the kingdom’s output to 9.7m b/d, its highest level in decades. But it claims to be able to pump as much 11m b/d, and further expansions to that capacity are supposed to be ready imminently. If King Abdullah really wants to deflate the oil markets, he could try announcing an increase in output of a few million barrels a day.

It is hard to know why Saudi Arabia does not do so.

Actually it is not hard at all. As has been discussed here, repeatedly, the excess oil that Saudi Arabia has for sale is heavy and sour and is not desired or usable by the market at the price that it being offered for.

But that is, in a way, a digression from my over-riding concern, which is illustrated by the example I gave at the beginning. Those who are asked about the causes and solutions to the current and increasing gap between demand at a reasonable price and liquid fuel supply tend to give answers based on their past experience and areas of knowledge. Thus, for example, you talk to those with a background in oil production, and they have always in the past been able to find and produce more to meet market demand, and so their answer is along the lines of “increase drilling and exploration.”

In the main folk tend to fall back on these answers since it is more comfortable to anticipate that this situation is a repeat of what has happened in the past, and it is more comfortable assuming that this is just another situation that will work out alright, since supply problems have been resolved in the past (so maybe the Economist quote is relevant). Unfortunately this time the problem is different. Because as we reach peak oil, and start to look at the down-side of that mountain of production, it is the length of the plateau at the top, and the rate of collapse beyond it, that should be recognized. This time around, the problem is sufficiently different that the solutions that have worked in the past are no longer valid.

Time to find new answers, as they say, is a’wasting – as the scale of the problem continues to be ignored by all but a few. But to address the consequences of the upcoming lack of oil is to recognize that the current state of business as usual cannot continue. It is to ask and debate the questions with uncomfortable answers, and where, of most commentators were honest, we don’t really know a lot of the answers. I am not sure that we even know all the questions that we should be seeking to answer.

The real issues of concern relate to such questions as “how long do we have until the situation really starts to deteriorate?” Some would say that it already is, and then there is the issue of “how rapidly will it deteriorate?” There is evidence from a number of fields that where horizontal wells predominate, that the decline in production, when it comes, will exceed 10% in such fields. Yet we accept 4 – 4.5% because that has been the historic number, and it gives us a more comfortable answer to questions like these, even though more and more fields are using horizontal wells and MRC technology. And so we continue, with the MSM really skirting the issues that should be more frequently discussed, because, unlike the movies that have been made on the oil supply situation, it is, in reality unlikely to result in a happy ending, at least in the intermediate term. It is easier and more comfortable to be out in the light, talking about the daily variations in oil prices, than it is groping in the dark trying to see what we are going to have to do to find an adequate supply of liquid fuels to meet the worlds needs – unfortunately it is in that unknown that the answers lie. It is still a relatively lonely place – there are not that many people looking there for answers yet, in fact there are disturbingly few.

[From Answering the Comfortable Questions about Energy]

Subscribe to:

Comments (Atom)